Imagine this: you’re sipping your morning coffee, sorting through the daily influx of mail, when a letter catches your eye. It promises to help you manage your credit card debt and save thousands of dollars. Intrigued? You’re not alone. Today, we’re diving into the nitty-gritty of a direct mail piece from Americor Financial. We’ll unravel its secrets, evaluate its legitimacy, and even share some laughs along the way. Buckle up, because this journey through the world of debt relief promises to be as entertaining as it is informative!

Step Right Up: Introducing Americor Financial

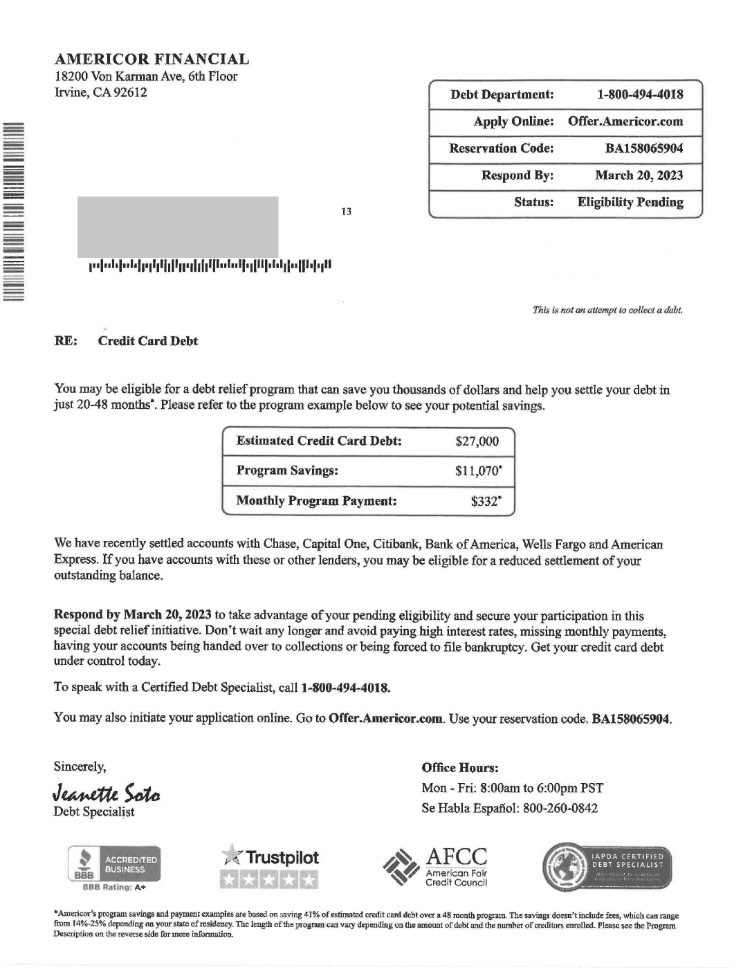

First things first, let’s get acquainted with our protagonist: Americor Financial. Based in sunny Irvine, California, Americor is a company dedicated to providing debt relief services. Their address, 18200 Von Karman Ave., 6th Floor, Irvine, CA 92612, is prominently displayed on the mail piece. It’s a solid start – after all, transparency is key in the world of finance.

Their contact details are as clear as a bell. They provide a phone number (1-800-494-4018) and an online application link (Offer.Americor.com). If you’re already feeling a bit of relief knowing there’s a way out of your debt maze, you’re not alone. But hold your horses! We need to dig deeper.

The Claims: Is It Too Good to Be True?

Now, let’s talk about the tantalizing promises made in this mail piece. It boasts of a debt relief program that can save you thousands of dollars and help you settle your debt in just 20-48 months. It even throws in a sample scenario showing a potential savings of $11,070 on an estimated credit card debt of $27,000, with a monthly program payment of $332.It sounds like a dream come true, right? But, as with all dreams, it’s wise to tread carefully.

The mail piece is quick to clarify that “This is not an attempt to collect a debt.” Instead, it’s an invitation to explore debt relief options. It’s worth noting that while urgency is a common marketing tactic, with a “Respond By: March 20, 2023” deadline, it doesn’t necessarily scream “scam.” But we’re not done yet.

Fine Print: Reading Between the Lines

Ah, the fine print – the tiny text that can make or break a deal. Here’s where Americor Financial lays out the terms and conditions. They’re upfront about program savings and payment examples being based on specific assumptions, and they mention that savings do not include fees, which can range from 14%-29% depending on your state of residency. So far, so good. There are no hidden fees here, just good old transparency.

But what about those recurring charges? Well, they’re mentioned too. The program length can vary depending on your debt amount and the number of creditors. Americor’s honesty about these details is commendable, but it’s always wise to read every word carefully.

Clear as Day: Clarity and Transparency

Let’s move on to the clarity of the message. The offer is straightforward, detailing potential debt relief savings and the monthly program payment. The call-to-action is clear and concise: call a phone number or visit a website with your reservation code. No rocket science here, just plain, understandable instructions.

The benefits (debt relief savings) and costs (monthly payments, program fees) are laid out plainly. The fine print and website information offer additional insights into risks and conditions, such as the potential impact on your credit and tax implications of forgiven debt. Kudos to Americor for keeping things transparent.

Who’s the Lucky Target?

Now, let’s talk about the intended audience. This mail piece is aimed at individuals with significant credit card debt who are looking for a way out. The language is formal yet inviting, suitable for those who are likely stressed about their financial situation. It’s a delicate balance, but Americor nails it.

The offer is relevant and valuable to those struggling with debt. If you’ve got credit card debt that keeps you up at night, this mail piece speaks directly to you. It’s like Americor has a sixth sense for finding people in need of financial relief.

Playing by the Rules: Compliance Check

In the wild world of finance, compliance with laws and regulations is crucial. This mail piece includes necessary disclaimers, such as “This is not an attempt to collect a debt,” and details about program savings and conditions. It mentions affiliations with AFCC and IAPDA, which indicates adherence to industry standards. So far, Americor seems to be playing by the rules.

The Advertiser’s Playbook

From an advertiser’s perspective, this direct mail piece is a home run. It’s professionally designed, with clear contact information and a compelling call to action. The estimated savings and payment examples provide tangible benefits that could persuade recipients to take the next step.

But what about brand alignment? Americor Financial positions itself as a savior in the debt relief industry, and this mail piece reflects that brand image perfectly. It’s all about helping people achieve financial freedom, and the tone and design reinforce this message.

Room for Improvement: Making It Even Better

No piece of marketing is perfect, and there’s always room for improvement. Here are a few suggestions:

- More Emphasis on Risks:

- While the mail piece does mention potential risks in the fine print, highlighting these more prominently could enhance transparency. For instance, a clear statement about the impact on credit scores and the potential tax implications of forgiven debt could be beneficial.

- Include a QR Code:

- In today’s digital age, convenience is king. Adding a QR code that takes recipients to the application page could improve user experience and response rates.

- Testimonials:

- Including testimonials from satisfied customers could add a personal touch and build trust. Hearing success stories from real people can be incredibly persuasive.

Conclusion: The Final Verdict

In the end, Americor Financial’s direct mail piece is a well-crafted, transparent, and effective marketing tool. It targets the right audience, provides clear and relevant information, and adheres to industry standards. While it’s important to approach any financial offer with a healthy dose of skepticism, this mail piece stands out as a legitimate and potentially beneficial option for those struggling with credit card debt.

So, the next time you’re sifting through your mail, watch for that letter from Americor Financial. It might just be the first step towards reclaiming your financial freedom. And remember, in the world of debt relief, a little knowledge goes a long way. Stay informed, stay cautious, and most importantly, stay hopeful. Financial peace of mind might be just a phone call (or website visit) away!

Frequently Asked Questions About Americor Financial

1. What types of debt does Americor Financial help with?

Americor Financial specializes in helping clients with various types of unsecured debt. This includes credit card debt, medical bills, debt consolidation, and certain types of private student loans. They work with clients to create personalized debt resolution plans aimed at reducing the overall debt burden and making repayment more manageable.

2. How does the debt resolution process at Americor Financial work?

The debt resolution process at Americor Financial typically involves several steps:

- Initial Consultation: Clients start with a free consultation to assess their financial situation and determine eligibility for the program.

- Customized Plan: Based on the client’s debt and financial goals, Americor creates a personalized debt resolution plan.

- Savings Account: Clients are advised to deposit funds into a dedicated savings account, which will be used to negotiate settlements with creditors.

- Negotiation: Americor’s team negotiates with creditors to settle debts for less than the full amount owed.

- Settlement and Payment: Once a settlement is reached, the client approves the agreement, and funds from the savings account are used to pay the agreed-upon amount.

3. What are customers saying about their experience with Americor Financial?

Customer reviews for Americor Financial are generally positive, with many clients praising the company for its professional and supportive staff. Clients often highlight the clarity and effectiveness of the debt resolution plans, as well as the relief they feel after reducing their debt burden. However, as with any service, experiences can vary, and some clients may encounter challenges depending on their unique financial situations.

4. Are there any upfront fees for Americor Financial’s services?

Americor Financial does not charge upfront fees for its debt resolution services. Fees are only charged when a debt is successfully settled, ensuring that clients only pay for results. These fees are typically a percentage of the debt enrolled in the program, which is communicated to clients during the consultation and agreement process.

5. How long does it take to see results with Americor Financial’s debt resolution program?

The timeline for seeing results with Americor Financial’s debt resolution program can vary depending on the client’s situation, including the amount of debt and the number of creditors involved. On average, clients may start seeing settlements within the first 3–6 months of enrollment. The entire program typically spans 24-48 months, during which time clients make regular deposits into their dedicated savings account to fund settlements.