If you’ve received a pre-approved loan offer from Bliss Financial in your mailbox, you might be wondering if it’s legitimate or if there are hidden pitfalls. These direct mail offers often promise attractive terms like low interest rates and high loan amounts – in this case, up to $100,000 at rates as low as 6.99%. But before you call that toll-free number or visit their website, it’s worth taking a closer look at what these offers really mean and how they work.

What is Bliss Financial?

Bliss Financial Corp appears to be a direct mail lead generation business based in Des Plaines, Illinois. According to information found online, they specialize in targeted leads for lenders in the financial industry rather than providing loans directly themselves. The company became BBB accredited in March 2024 and presents itself as a connector between potential borrowers and actual lenders.

Understanding Pre-Approved Mail Offers

When you receive a “pre-approved” offer in the mail, it’s important to understand what this actually means. These offers are often based on limited information about you that was purchased from credit bureaus or obtained from public records. The term “pre-approved” can be misleading – it typically means you’ve met some initial screening criteria, not that you’re guaranteed to receive the advertised loan terms.

Red Flags to Watch For

1. The Bait and Switch

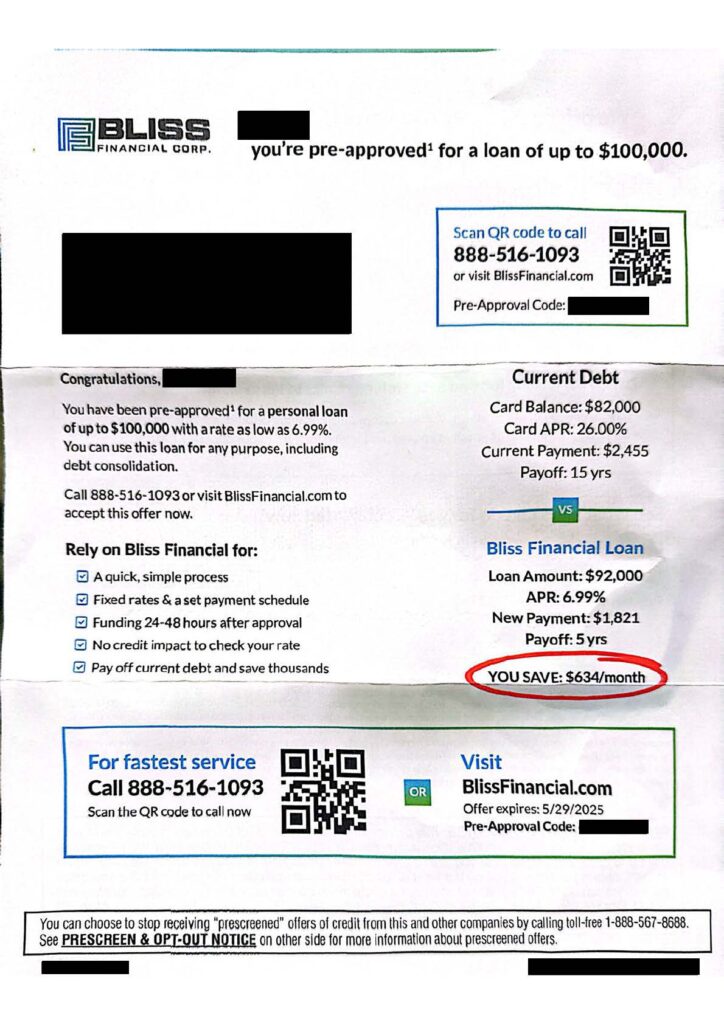

One common tactic used by some loan marketing companies is advertising extremely favorable terms that very few applicants will actually qualify for. The eye-catching low interest rate of 6.99% prominently displayed on the Bliss Financial mailer is likely the absolute best-case scenario reserved for borrowers with excellent credit and income. Most applicants may be offered significantly higher rates.

2. Lead Generation vs. Direct Lending

Bliss Financial doesn’t appear to be a direct lender but rather a lead generator. This means when you respond to their offer, your information will likely be shared with multiple third-party lenders or partners. This can sometimes result in a flood of calls, emails, and additional offers from various companies.

3. Fine Print and Hidden Fees

The promotional material shows the potential monthly savings ($634/month) prominently circled in red, creating a sense of urgency and excitement. However, the actual loan terms, potential fees, and conditions may be buried in fine print. Origination fees, application fees, or prepayment penalties could significantly impact the true cost of the loan.

4. High-Pressure Sales Tactics

Some financial marketing companies may use high-pressure tactics once they have you on the phone. They might create artificial deadlines or claim the offer is about to expire to push you into a quick decision before you’ve had time to fully review the terms or shop around.

How to Evaluate the Offer

1. Research the Company

Before responding to any loan offer, research the company online. Look for reviews, complaints, and their reputation with consumer protection agencies. While Bliss Financial has some positive reviews on platforms like Trustpilot, it’s always good to get a complete picture by checking multiple sources.

2. Read the Fine Print

The mailer does include a footnote with the number “1” next to “pre-approved,” which suggests there are conditions or qualifications attached to this approval. Always read all the fine print and disclosures carefully before proceeding.

3. Compare with Other Options

Even if the offer is legitimate, it may not be the best deal available to you. Before accepting any loan offer, shop around and compare rates, terms, and fees from multiple lenders. Many banks, credit unions, and online lenders can provide pre-qualification without affecting your credit score.

4. Understand the Debt Consolidation Math

The mailer shows a comparison between current credit card debt ($82,000 at 26% APR with a $2,455 monthly payment and 15-year payoff) and their proposed loan ($92,000 at 6.99% with a $1,821 monthly payment and 5-year payoff). While the monthly savings look substantial, note that the loan amount is higher than the current debt, which raises questions about additional fees or inclusion of other debts not clearly explained.

The Bottom Line

While pre-approved loan offers like the one from Bliss Financial aren’t necessarily scams, they often present best-case scenarios that may not reflect the actual terms you’ll be offered. The Consumer Financial Protection Bureau advises consumers to be cautious with unsolicited loan offers and to thoroughly review all terms before proceeding.

If you’re considering debt consolidation, it may be more beneficial to work directly with established financial institutions or reputable online lenders that can provide transparent terms upfront without the pressure tactics sometimes associated with direct mail offers.

Remember, you can opt out of receiving pre-screened credit offers by visiting optoutprescreen.com or calling 1-888-567-8688, a service run by the major credit bureaus.

What to Do If You’ve Already Responded

If you’ve already called the number on the Bliss Financial mailer or shared your information:

- Ask for complete written terms before agreeing to anything

- Take time to review the actual offer carefully

- Don’t feel pressured to make an immediate decision

- Consider consulting with a financial advisor if the terms seem complex

Making informed financial decisions takes time and research. When it comes to significant financial commitments like debt consolidation, it’s always better to proceed with caution rather than rushing into a decision based on a persuasive marketing piece that arrived in your mailbox.